Welcome back to LiST’s life insurance blog.

Last week we discussed which basic information appears on the annual statements and got a general understanding how permanent life insurance works. Now that we know what the death benefit is, and that the policy is split into a cash and insurance component, we will dig down into how the cash component increases (or decreases).

First, payments are made to the carrier by the insured. These payments are called premiums and can generally be made at different intervals (monthly/quarterly/semi annually or annually). Certain policies require a minimum premium to be made (more about this later), but most policies are flexible, and the premium amount can vary.

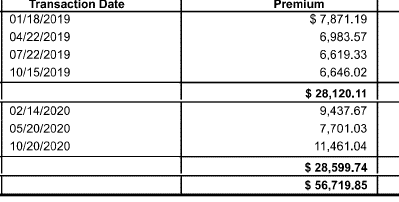

The premiums paid into the policy over its lifetime (from inception to death-just like people) may appear in the annual statement, such as here:

Or alternatively, may only be available in a separate document- the premium history, which looks like this:

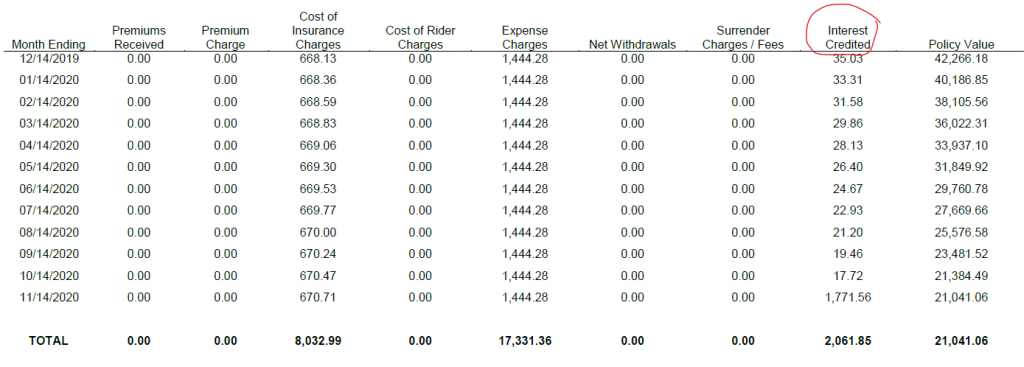

Money comes in, but money also goes out. Policies have many fees (some of which are hidden), and we will discuss them in our next blog. After the fees are deducted, the remaining amount of premium payment less fees, plus the cash value from previous years, will start earning cash in one of the following ways:

This interest/investment amount is added to the cash value of the policy, and can be seen here:

The premium payment information is very important and should be marked and filed. It can impact whether your client meets the taxman if they choose to discontinue their policy.

Join us again next week.

The contents do not constitute legal advice, are not intended to be a substitute for legal advice and should not be relied upon as such. You should seek legal advice or other professional advice in relation to any particular matters you or your organization may have.

Disclaimer:

Neither List Funding Inc nor its affiliates and subsidiaries (collectively, “List”) are registered as a licensed broker-dealer and/or as Life Settlements brokers or provider. List does not advise on any sort of investment and does not make any representations or warranties as to the legality of any investment. All decisions to invest are the sole responsibility of the individual investors. Moreover, List does not provide financial, legal, accounting or tax advice. Such advice, including investment advice, should be obtained from professionals who understand the ramifications of investments such as those featured on the List website. The information on our website and/or in any other materials supplied by List do not purport to include all of the information necessary to evaluate an investment and are qualified in their entirety by the terms of any offering materials along with the transaction documents (i.e., form of subscription agreement, terms and conditions, etc.) that are associated with an investment. No offer or sale of any securities will occur without the delivery of confidential offering materials and related transaction documents. Accordingly, the List website is merely intended to provide general information and is intended for initial reference purposes only. There may be advantages and disadvantages that vary depending upon the circumstances of a particular case, and nothing on the List website and/or other materials is intended to be relied upon by any prospective investor. Neither the Securities and Exchange Commission nor any federal or state securities commission or any other regulatory authority has recommended or approved any investment or the accuracy or completeness of any of the information or materials provided by or through the List website.

Private placements on List are intended for accredited U.S. resident investors and for sophisticated investors residing abroad in jurisdictions where securities registration exemptions are available. Securities sold in private placements are not publicly traded, are subject to holding period requirements, and are intended for investors who do not need a liquid investment. Private placement investments are NOT bank deposits (and thus NOT insured by any federal governmental agency), are NOT guaranteed by List or any other party, and MAY lose value. Investments of this sort are speculative and involve a high degree of risk and those investors who cannot afford to lose their entire investment should not invest.

This disclaimer is further qualified by, and subject to, List Funding’s

Looking to invest in the Life Settlements Market in an efficient and transparent way

Looking to eliminate monthly premiums and maximize asset value