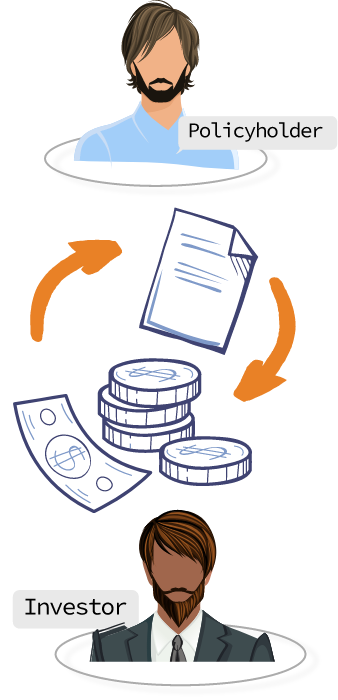

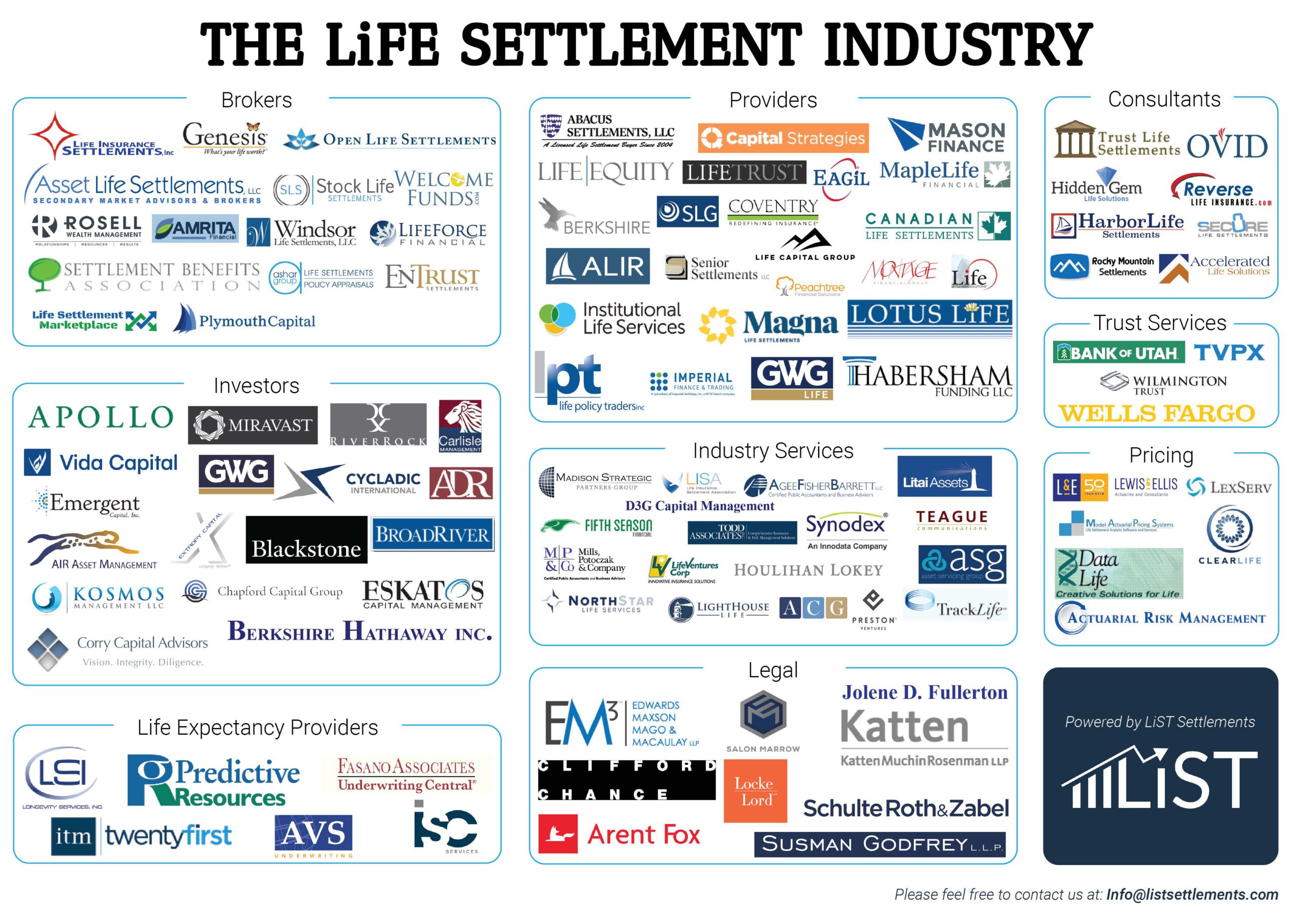

Policyholder – a person or persons who own a life insurance policy.

Life Settlements Investor – an individual or group of individuals who purchase life insurance policies from policyholders.

Life Settlements financial firms – firms engaged in Life Settlements investments. Regulations prohibit direct buying from policyholders – companies may only buy through providers.

Life Settlements broker – a state licensed agent representing sellers in Life Settlements transactions.

Life Settlements provider – a state licensed agent representing buyers in Life Settlements transactions and handling the procedure of ownership transfer.

Life expectancy provider – actuarial firms engaged in life expectancy evaluation.

Pricing provider – policy pricing firms.

Legal firms – law firms specializing in Life Settlements.

Trust services – assets are usually held by trust services.

Consultants – these are usually people who support the policy sellers but do not have a broker’s license.

Industry services – firms that provide various ancillary services in this industry.

LiST – Next-gen asset management powered by data.

{kind=link}