These statements are released on an annual basis by life insurance carriers. While it may look like pure Chinese (or Legalese), the annual statement is generally straightforward and includes the following information:

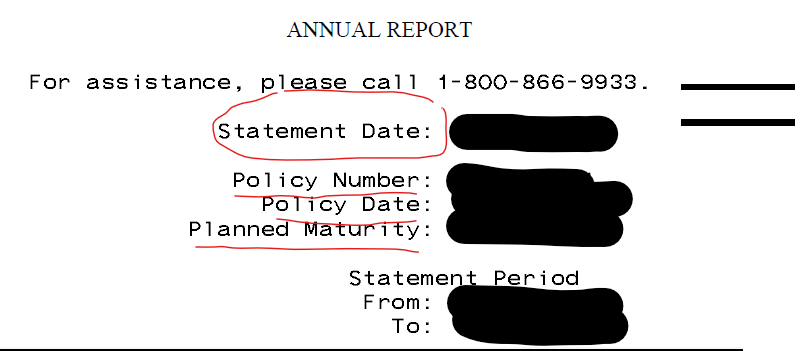

- Basic information about the policy, including the policy number (which can be used to reference the policy), the policy issue date (when the policy was issued- AKA “the policy anniversary”), the statement date (when the statement itself was issued) and the planned maturity date (when the policy is projected to lapse, if the policyholder does not pass into the gates of heaven/hell (if you have any clients who are lawyers) beforehand).

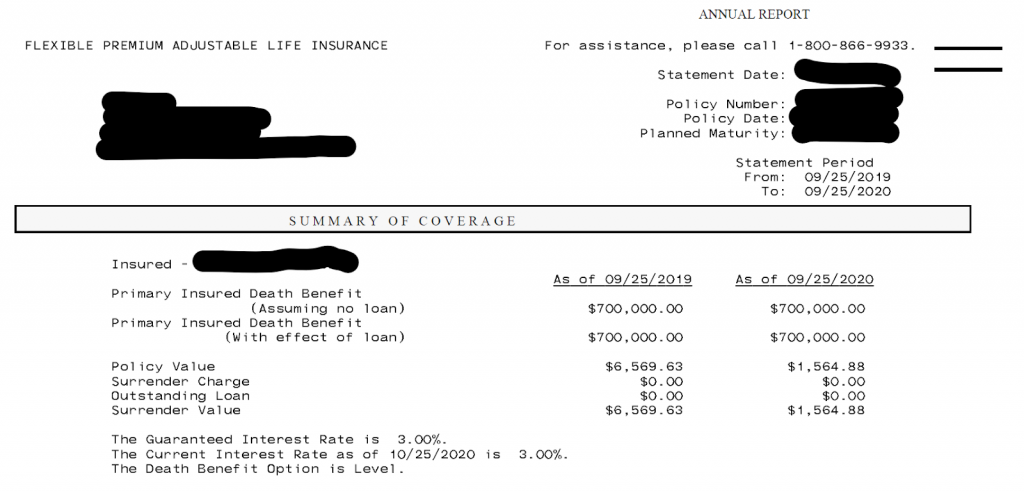

- Next, we can see what the current death benefit is (the cash that your client’s loved ones will receive after their passing). If your client took a loan against the policy, this amount will be deducted (pound of flesh and all) from the death benefit amount. Statement without a loan:

This is how the statement looks if there is a loan:

This is how the statement looks if there is a loan:

- After understanding the death benefit amount and the policy dates, you are ready for the next stage (welcome to the big leagues). Now is time to dig in briefly to understand how permanent insurance policies are built. As opposed to term policies, which are pure insurance, many permanent life policies are comprised of insurance (risk) and a savings account.

The savings account is generally called “cash value” or “account value”, which is built up in the policy over its lifetime. This value may withdrawn from the policy (see more in future blogs). In this case, there is generally a certain withdrawal fee (“surrender fee”), usually if the policy is surrendered over a certain period. After this period, the fee generally drops or goes down to zero. The cash value amount, net of the fee, is called the cash surrender amount or net surrender value.